I thought I would post up a quick posting on when you should update your will or trust:

If you move to a new state – you should see if it requires updated estate planning documents

If you Get Married or Divorced – You might need an estate planning update

If you have a new child – you might need an update to your estate plan

If the law has changed or there is a significant change in financial circumstances you might need an update.

If you want to change beneficiaries or guardians or trustee

The tricky one is #4, so in general if you have not met with an estate planning attourney in several years, it would likely be a good idea to schedule a meeting and determine if you are due for an update.

** The information on this website is intended only for informational purposes. Investors should not act upon any of the information here without performing their own due diligence. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.

I would like to thank Ann Garcia CFP® for writing this very informative article on education planning. Ann Garcia, CFP®, is a fee-only financial advisor with Independent Progressive Advisors and author of The College Financial Lady blog. Thanks again Anne! – Steve Reh

When it comes to college savings, the tax benefits of 529 plans are pretty well-known: tax-free growth and withdrawals and in some states, a tax deduction on contributions. Many people, especially those in states that don’t grant a tax deduction for contributions, believe that tax-efficient investments in a taxable account are just as good a college savings option.

Ann Garcia CFP® – Secret 529 Plan Bonus

But 529 plans have another, far less well known but potentially much more significant, advantage over taxable accounts when it comes to college savings. To understand that benefit, you first need to understand the financial aid formulas that colleges use.

Financial Aid Formulas

Eligibility for need-based college financial aid is determined based on the student’s Expected Family Contribution, or EFC. There are two methodologies for calculating EFC: the federal methodology which uses the FAFSA form, and institutional methodology using the CSS PROFILE. There are similarities and differences in these forms; for the purpose of this analysis we’ll use the FAFSA methodology because it is more transparent, and for purposes of this discussion it’s reasonably similar to the CSS PROFILE. Keep in mind that about 70% of college students receive some form of financial aid. Even though a good amount of that is merit aid which typically does not consider ability to pay, need-based aid is granted to students coming from families with household incomes approaching $200,000 annually.

The Four Factors of the Expected Family Contribution (EFC)

Four factors go into the EFC: parents’ income and assets and student income and assets. Each of those has a different formula applied to it to determine how much is “available” to pay for college. The formulas generally assume that students have nothing better to do with their money than pay for college, so their income and assets are assessed far more than parents’: 20% of their assets—including checking and savings accounts—are considered available for college and 50% of their income over about $6,000.

Parents, on the other hand, are assumed to have other uses for their money so they get more favorable treatment. The formulas offer (limited) allowances against income (approximately equal to the federal poverty level) and assets (usually around $20,000 for married parents; considerably less for single parents). Several adjustments are made to income—most significantly, income taxes paid are subtracted from income and pre-tax retirement contributions are added back—and the remaining amount, the “adjusted available income,” is assessed in various brackets, much like income tax brackets. The top rate of 47% kicks in at about $32,000 of available income. Parents with household income of around $100,000 could expect their contribution from income to be around $17,500.

Parent assets—including 529, taxable investment, checking and savings accounts but not retirement savings accounts—are given much more favorable status. Only 5.64% of assets above the asset protection allowance count towards the EFC. $100,000 in savings for education—regardless of account type—would only increase EFC by about $1,125. Again, no matter whether the money is in a 529 account or a taxable brokerage account.

The 529 Plan Asset Distribution Advantage

Once you try to use your savings for college expenses, though, the 529 plan becomes vastly superior to the taxable account. That’s because you don’t have to report the gain in the account as income when it’s distributed, either in your tax filings or on the FAFSA. Here’s a simplified example of how that works. Let’s say you are going to use $25,000 from your savings to pay for freshman year of college. You started saving early and your account has doubled in value while you’ve held it, so your basis is $12,500 and your gain (long term) is $12,500. If you took that money out of your 529 account, you would have $25,000 to spend for college, and the following year your EFC would decrease by $25,000 x 5.64% or $1,410.

If you took it out of the taxable account, you’d report that $12,500 as income next time you file the FAFSA. Assuming you already had $32,000 in other available income, this withdrawal would increase your EFC by about $4,500 net of the withdrawn amount.

529 Plan’s Advantage over Roth IRAs

You may be looking at this and thinking, “Why do either of these? Instead, I’ll use a Roth IRA. I don’t have to report it as an asset, plus I get tax-free withdrawals!” The obvious reply to that is, a Roth IRA is for retirement, not college. Setting that aside, Roth IRAs have a bigger drawback than taxable accounts when used to pay for college: even though the distribution may be tax-free, it still must be reported as income on the FAFSA. In that case, even though none of it may be taxable, 100% of the distribution is considered income for FAFSA purposes. That means your $25,000 withdrawal increases your EFC by $11,750.

All in all, parents of college-bound students are far better served by a 529 plan than any other savings vehicle. Your financial advisor can help you find the best plan for your family’s circumstances.

As a continuation of the Fee-Only Financial Advisor blog sharing group, this month’s post comes to us from Michael Garry, a Financial Advisor in Newtown, PA.

“Two roads diverged in a wood, and I—

I took the one less traveled by,

And that has made all the difference.”

–Robert Frost, excerpt from the Road Not Taken

Whether you think this poem is about individualism or rationalization, you surely know the poem and how it is commonly construed.

An article was recently published in Financial Advisor Magazine examining the various regrets that people commonly have and one of them was avoiding risks. A quote from the article summarizes this common regret well: “Among the top regrets were: not following their dreams, not taking risks with their careers, not taking risks with their lives in general, and not being gutsy enough in the choices they made.”[i]

Although this could sound depressing, many people that were consumed by these feelings of regret were determined to fix this by taking more risks with the time they have left. It’s a good attitude to have.

Ninety-three percent of Americans have a favorable view of an extended life with the feeling it could open new and interesting possibilities

Nearly half feel a longer life can enable a totally different view of how and when major life choices are made

A longer life is going to require some different approaches to financial planning.

As a financial advisor one of my main goals is to empower people to take risks in their lives, and lead the lives they imagine, by giving them peace-of-mind with their finances.

It is common for people to feel overwhelmed and uncertain in terms of their financial future and unfortunately, this paralyzes them in other parts of life. People have certain goals/dreams, or simply things they need that they view as unattainable because they feel limited by lack of resources or organization.

Financial plans and investment strategies allow you to determine achievable goals and establish a detailed plan for reaching them. Further, with a clear idea of what resources are available to you and how you can use those resources, you can shift your current financial situation to one that is aligned with your goals and future.

Everyone is unique – simply because one person handled their financial situation one way does not mean that you must do the same. Everyone should accept the challenge of discovering their individuality and embrace it in a way that will aid them in reaching their goals for the future.

Taking the road less traveled, taking risks, living life to the fullest and making your goals a reality may sound like lofty naiveté, but it’s not.

“I would to Thank Dave Fernandez, CFP® of http://www.wealth-engineering.com/ for contributing his expertise on 401(k) and the options you have when you leave your employer” -Steve Reh

401(k) Options When You Leave Your Employer

Guest Blog Article by Dave Fernandez about your 401k Options when you leave your employer.

Regardless if you are retiring or moving to a new employer, once you leave your current job you will need to decide what to do with your 401(k). You have a handful of choices. I have outlined the benefits and disadvantages of each option below. Your personal circumstances may favor one option over the other. You should discuss your options with a fee-only financial advisor whenever you transition employment so he/she can help you determine which pathway provides the best choice for your unique financial situation.

1) If you have a balance of $5,000 or greater you can likely leave it in your current plan as most 401(k)’s provide a deferral option.

Benefits –

This is the easiest decision and likely no action is required on your part. Although, I am always amazed how many investors choose this default option when there are better choices as described below.

Disadvantages –

Every 401(k) plan has its own unique set of investment options. Your current plan may have a limited choice of investment options such as being overly U.S. centric. We live in a global economy and most financial advisors recommend that portfolios should provide a decent amount of international options on both the stock and bond side of investment choices.

Many 401(k)’s have incredibly high internal expenses. It is not uncommon to see mutual fund choices with expense ratios north of 1.5%. It is very important to keep an eye on your overall investment expense exposure. The more you can lower your investment expenses, the higher probability you can keep returns compounding for your long-term financial benefit.

Be aware that if your balance is less than $5,000, you will want to take action on one of the below choices as your employer may have the option to automatically cash your 401(k) account out or transfer you to an IRA. Cashing your 401(k) account out can have large tax consequences as outlined later in this article.

2) Rollover your balance to your new employer’s 401(k) plan.

Benefits –

This is a good way to consolidate financial assets, especially if you have more than one 401(k) from past employment. I always favor consolidation and simplification where possible.

This could be a great choice if you have an excellent set of diversified investment options that are low cost.

Disadvantages –

It is not uncommon for your benefits department at work to occasionally choose a new custodian or a new set of investment options in your 401(k) every few years. You have less control in this situation as you are forced to invest in whatever options are provided. What may look great today could easily change unexpectedly.

Your new 401(k) may have poor investment choices, and/or investment options with high expenses.

Most 401(k) rollovers are initiated from the 401(k) you are leaving. Your human resources department or benefits office may require that you fill out a termination/rollover packet of paperwork. Some 401(k) custodians may take direction over the phone. Collectively you and your fee-only financial planner can determine what is the next step to move forward.

3) Rollover your 401(k) to an IRA

Benefits –

This is typically a favored option. Once you set up an IRA you have the whole investment universe of options to invest in. This could be mutual funds, ETFs or stocks. It is easy to build a well-diversified portfolio when you have such a wide array of investment options to choose from.

You have control over your money. You can always move your IRA to another investment custodian if you prefer a change of investment options.

You will have control over investment expenses. There are a number of low cost investment options available via no-load mutual funds and ETFs at a number of investment custodians.

Disadvantages –

If you are still working, you may end up with one extra investment account in a separate IRA. This is a minor disadvantage. The benefits of investment selection and cost control provided with rolling your 401(k) to an IRA easily outweigh the disadvantage.

4) Cash out your 401(k)

Benefits –

None, other than liquidity if you are in a situation desperate for cash.

Disadvantages –

This is typically the worst decision you can make as any balance withdrawn is a taxable withdrawal. Your 401(k) custodian is required to withhold 20% in federal taxes, but your tax exposure could be higher depending on your marginal tax bracket.

You will owe state income taxes on the withdrawal if you live in a state that taxes income.

If you are under age 59 ½ you would also be subject to a 10% early withdrawal penalty.

If you have an outstanding 401(k) loan balance, the loan would also become a taxable event and be subject to the taxes and penalties described above.

You will miss out on any future tax-deferred compounded growth by cashing out your 401(k) today.

There are a couple of other scenarios to be aware of before deciding on one of the above choices:

What if you have a loan balance against your 401(k)?

You typically have 60 days to pay back a 401(k) loan after leaving employment. After 60 days, your loan balance will likely be considered a taxable distribution and you will be subject to taxes and possibly a 10% early withdrawal penalty if you are under 59 ½ years old.

What if you have greatly appreciated employer stock in your 401(k)?

You may have a tax preference option called Net Unrealized Appreciation or NUA which allows you to transfer the stock out of the 401(k) and pay ordinary income taxes on the cost basis and capital gains taxes on the gains. You will want to review this option in detail with your financial advisor and CPA prior to making any decisions.

In closing, I highly recommend you notify your financial planner of any employment changes which could impact your 401(k) options. Once he/she is aware of your choices, they can help you determine what the best course of action is for your personal financial situation. You can always ask your financial advisor to join you in a conference call with your benefits department and/or 401(k) custodian to make sure you both understand all of your options and what steps are required to move forward.

About The Author

Dave Fernandez, CFP® is a native of Arizona and has over 20 years of experience in the financial services industry. He started his financial services career in 1995. As a NAPFA Registered Financial Advisor, Dave owns a fee-only financial planning and wealth management firm, in Scottsdale, Arizona called “Wealth Engineering.”

Update to the Article: 2015 Q3 Stock Market, Is it 2011 Q3 Again or 2008 Q3?

I realize that people are likely more interested in my opinion on the current market drop but I first want to revist our last market drop. I will have another article about our current market conditions soon.

What Happened in Previous Market drops of Q3 2011 and Q3 2008?

As a reminder here is the performance for the S&p500 in Q2 2008 and Q3 2011. An ugly 8.87% and an uglier 14.92% loss in 2011.

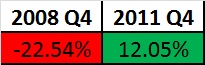

What Happened in Q4 2011 and Q4 2008?

And here is a reminder how Q4 went in both time periods.

Update – Let’s Look at 2015 Q4

Thankfully, the 4th quarter of 2015 looked a lot more like the 4th quarter of 2011.

As mentioned previously, 2008 tended to be an anomaly in that it was one of the worst years we have experienced in the stock market; certainly it was the worst of my lifetime. Our bias is to remember things we experience and give a greater likelihood of thinking it will occur again (the phenomena is called the “Availability Bias”). The Availability Bias is the bias that is how we estimate future probabilities based on how easy it is to remember. A good example would be our current drought in Southern California. Most Southern Californians would likely overestimate the probability of future droughts based on the ease they can remember our current drought.

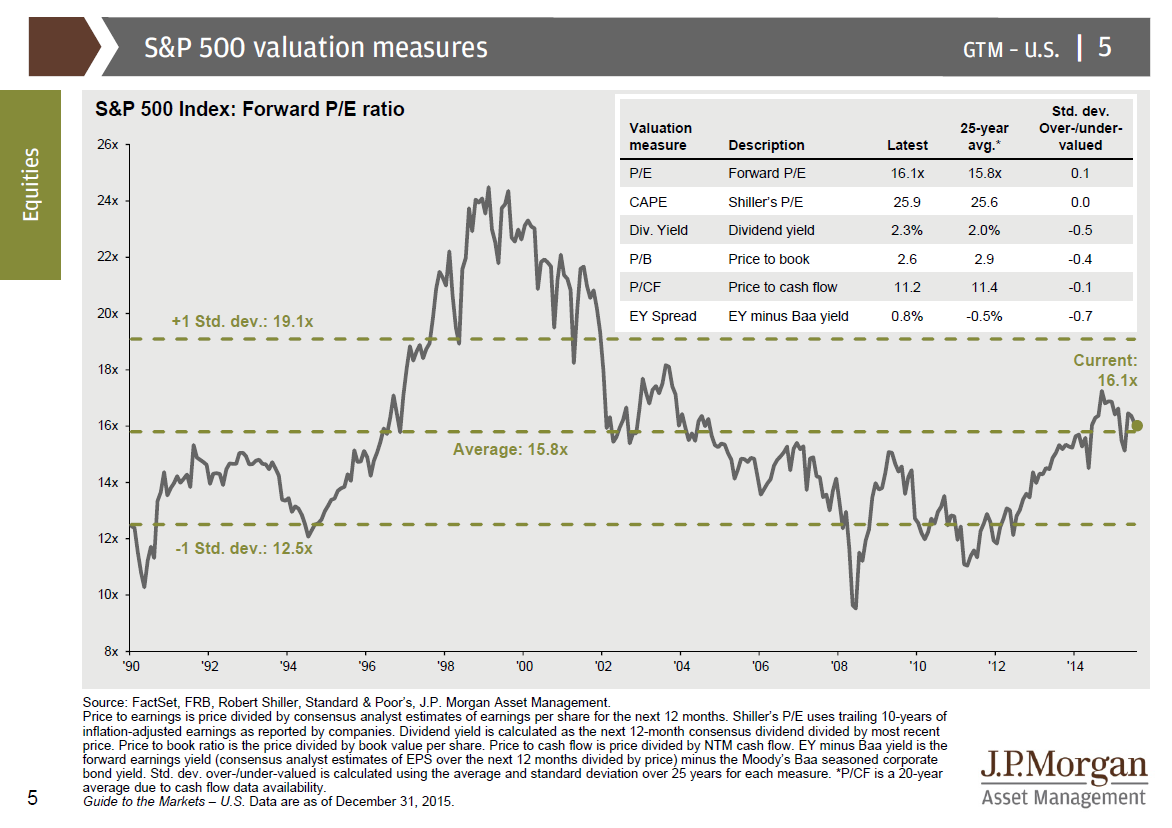

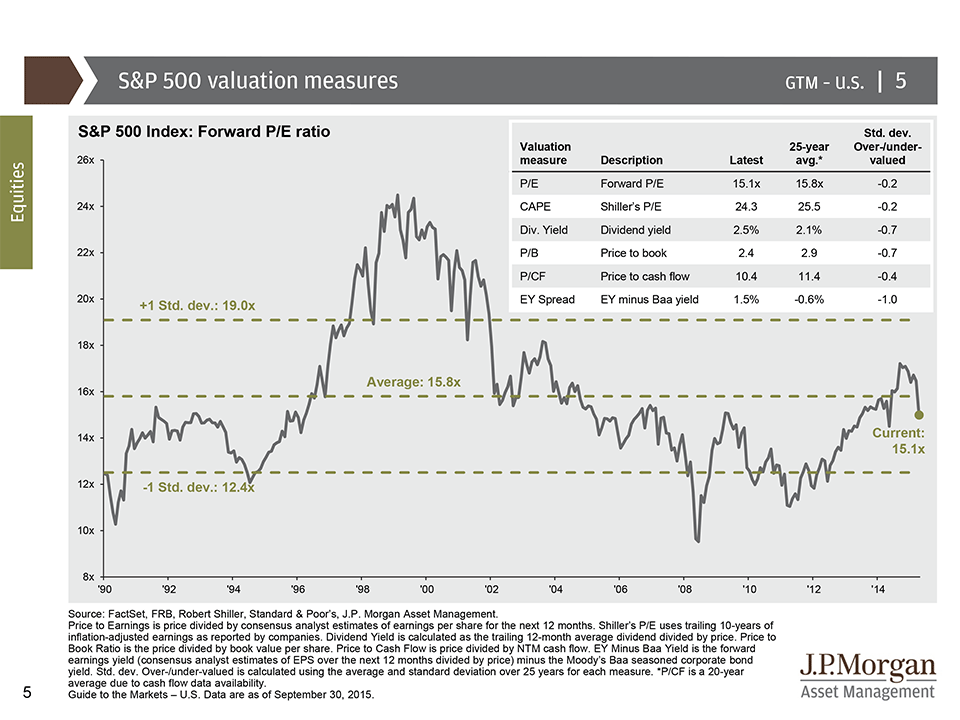

Where are we at a valuation Standpoint as of 12/31/2015?

The equity market does not appear to be valued too high or too low. According to the most recent data as of 12/31/2015 in the JP Morgan “Guide to the Markets”, most measure show that the market is fairly valued.

(Source: JP Morgan)

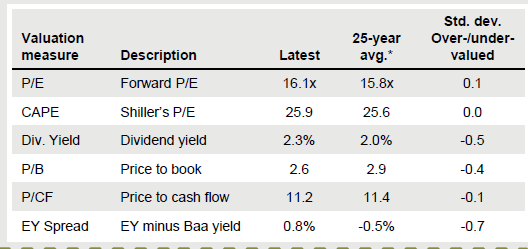

The P/E (Price to earning measure), CAPE (cyclically adjusted Price to earnings), and P/CF (Price to Cash Flow) all show a market that is fairly valued.

Dividend yield, Price to Book value, and Earning Yield less Baa Bond yield all show that the market is slightly undervalued currently.

So how do I feel about it currently? As I stated last quarter, I actually think the market is fairly valued and there is both upside and downside and I feel that our best course of action is a diversified portfolio. If valuation measure were dramatically different, I might feel otherwise.

What about the Bond market with the recent Fed Rate Increase? I am worried about the bond market but I think for investors in diversified portfolios, the fear is over blown. The Fed raised rates slightly but it the impact on bond prices was relatively tame. I think the Fed will be cautious about raising rates unless inflation kicks up.

What is our takeaway?

When markets misbehave (go down), we should look at times in history to see what happened. We should look at valuation ratios to see if the market is reasonably valued. In many cases, the best course of action is to 1) take tax losses if you can 2) rebalance if you are too far from your model 3) Trust your asset allocation and risk to prevent you from performance chasing.

** The information on this website is intended only for informational purposes. Investors should not act upon any of the information here without performing their own due diligence. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.

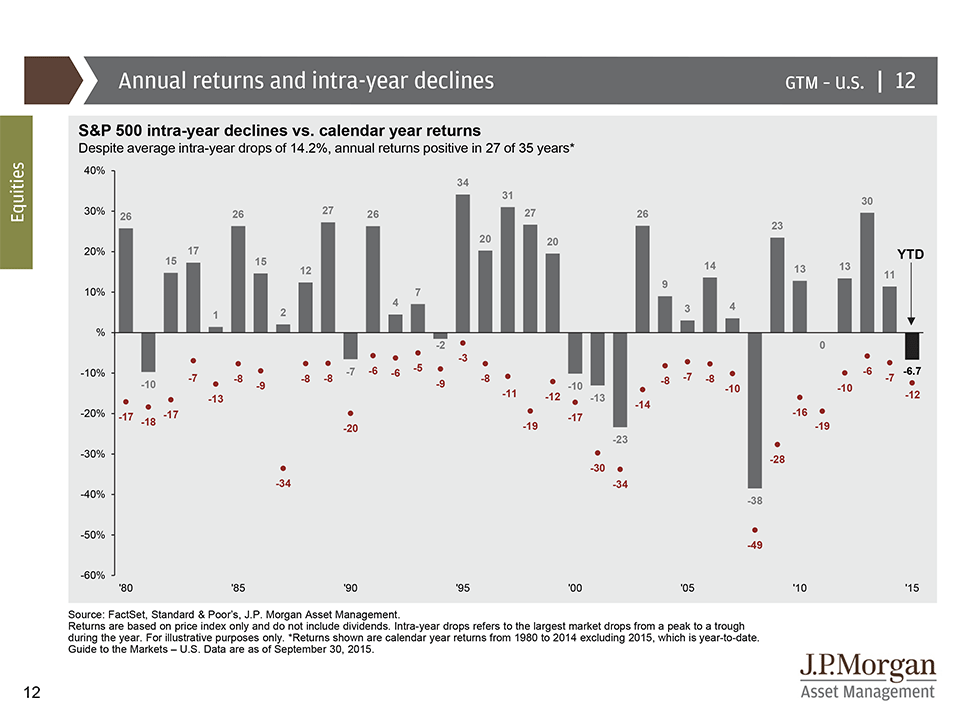

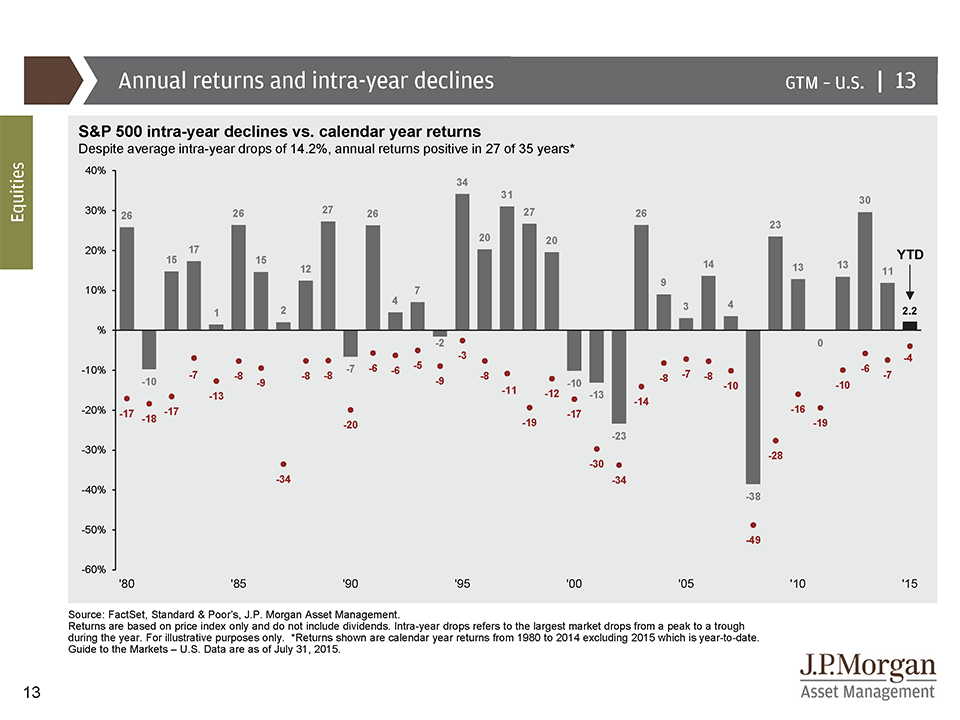

As we previously discussed, at that time through July 31, 2015 the market had only declined 4% from its market high. Due to a rough August and September, we can see the S&P500 declined 12% from its high:

That 12% drop is almost at the average intra year drop of 14.2%. As a reminder, we can see that despite several years were there were relatively large drop, many years still ended up being positive. That scenarios increases the risk that an investor might sell at the wrong time or may incorrectly time the market.

Current Valuation – the Market is still fairly valued

By looking at the major valuation metrics (P/E, CAPE, Div Yield, P/B, P/CF, and EY Spread), the market is slightly undervalued. Since its less than one standard deviation (far right column), I would actually classify this market as “fairly valued”. We are not seeing panic or greed driven values currently.

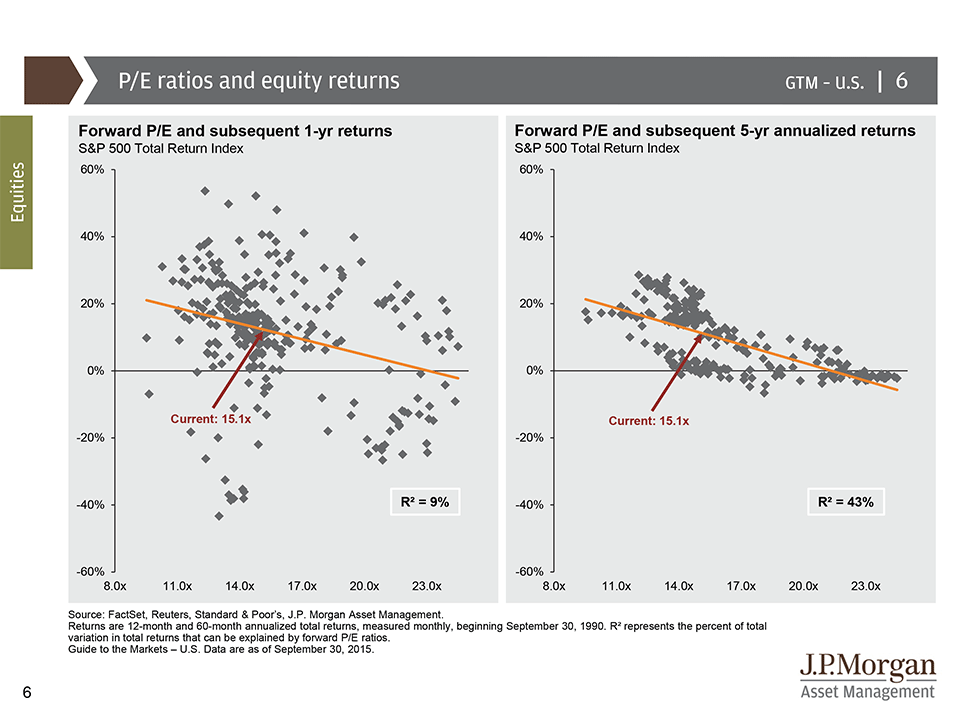

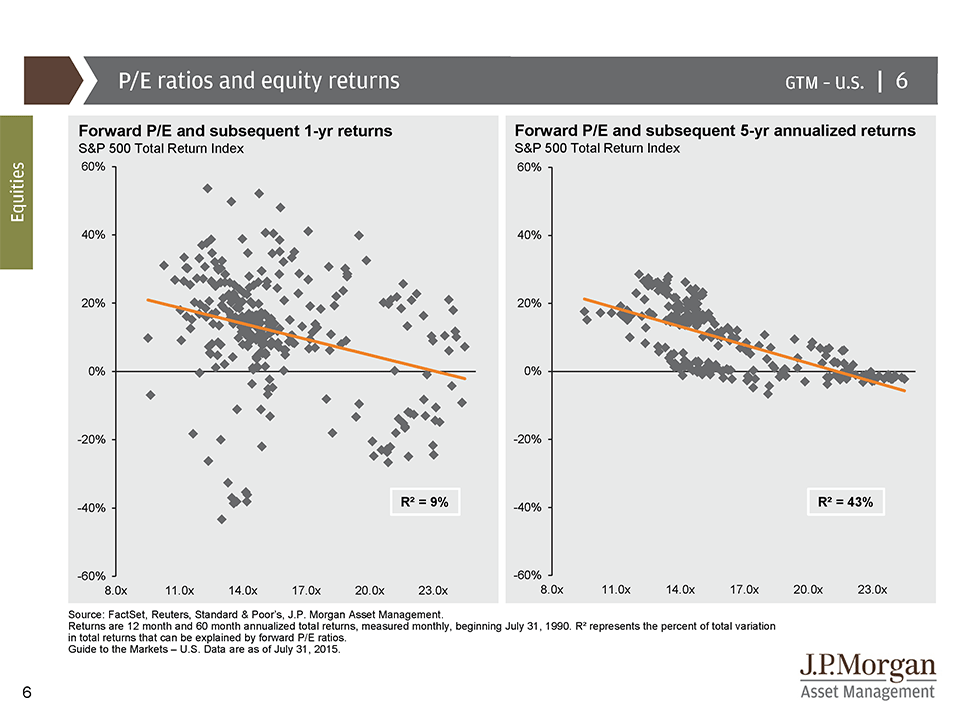

P/E Ratio is Poor Predictor of Short Term Performance but much better at Intermediate Performance

Although the model predicts good returns over the next year, the R Squared is only 9% so using P/E to predict the next 12 months is a dangerous proposition. It does show that according to P/E, we are not seeing a dramatically overvalued market. As we have discussed before, the 5 year performance based on P/E is much stronger with an R Squared of 43%. That means the current P/E can explain 43% of the next 5 years performance. The current P/E indicated the next 5 year should be good for the market.

I would like to thank JP Morgan for their always excellent quarterly guide to the markets where the slides came from.

** The information on this website is intended only for informational purposes. As always, past results do not guarantee future returns. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.

2015 Federal Tax Rates, Tax Tables, Personal Exemptions and Standard Deductions

This article gives you the tax rates and related numbers that you will need to prepare your 2015 income tax return. In general, 2015 individual tax returns are due by April 15, 2016.

$119,996.25 plus 39.6% of the amount over $413,200

Married Filing Jointly or Qualifying Widow(er):

Taxable Income

Tax Rate

$0 to $18,450

10%

$18,451 to $74,900

$1,845.00 plus 15% of the amount over $18,450

$74,901 to $151,200

$10,312.50 plus 25% of the amount over $74,900

$151,201 to $230,450

$29,387.50 plus 28% of the amount over $151,200

$230,451 to $411,500

$51,577.50 plus 33% of the amount over $230,450

$411,501 to $464,850

$111,324.00 plus 35% of the amount over $411,500

$464,851 or more

$129,996.50 plus 39.6% of the amount over $464,850

Married Filing Separately:

Taxable Income

Tax Rate

$0 to $9,225

10%

$9,226 to $37,450

$922.50 plus 15% of the amount over $9,225

$37,451 to $75,600

$5,156.25 plus 25% of the amount over $37,450

$75,601 to $115,225

$14,693.75 plus 28% of the amount over $75,600

$115,226 to $205,750

$25,788.75 plus 33% of the amount over $115,225

$205,751 to $232,425

$55,662.00 plus 35% of the amount over $205,750

$232,426 or more

$64,998.25 plus 39.6% of the amount over $232,425

Head of Household:

Taxable Income

Tax Rate

$0 to $13,150

10%

$13,151 to $50,200

$1,315.00 plus 15% of the amount over $13,150

$50,201 to $129,600

$6,872.50 plus 25% of the amount over $50,200

$129,601 to $209,850

$26,772.50 plus 28% of the amount over $129,600

$209,851 to $411,500

$49,192.50 plus 33% of the amount over $209,850

$411,501 to $439,000

$115,737.00 plus 35% of the amount over $411,500

$439,001 or more

$125,362.00 plus 39.6% of the amount over $439,000

2015 Personal Exemption Amounts

You are allowed to claim one personal exemption for yourself and one for your spouse (if married). However, if somebody else can list you as a dependent on their tax return, you are not permitted to claim a personal exemption for yourself.

For tax year 2015, the personal exemption amount is $4,000 (up from $3,950 in 2014).

The personal exemption amount “phases out” for taxpayers with higher incomes. The Personal Exemption Phaseout (PEP) thresholds are as follows:

Filing Status

PEP Threshold Starts

PEP Threshold Ends

Single

$258,250

$380,750

Married Filing Jointly

$309,900

$432,400

Married Filing Separately

$154,950

$216,200

Head of Hosuehold

$284,050

$406,550

2015 Standard Deduction Amounts

There are two main types of tax deductions: the standard deduction and itemized deductions. You can claim one type of deduction on your tax return, but not both. For example, if you claim the standard deduction, you cannot itemize deductions – and vice versa (if you itemize deductions, you cannot claim the standard deduction). You are allowed to use whichever type of deduction results in the lowest tax.

The standard deduction is subtracted from your Adjusted Gross Income (AGI), thereby reducing your taxable income. For tax year 2015, the standard deduction amounts are as follows:

Filing Status

Standard Deduction

Single

$6,300

Married Filing Jointly

$12,600

Married Filing Separately

$6,300

Head of Household

$9,250

Qualifying Widow(er)

$12,600

Please Note that Information Below these lines, refers to California Taxes, Rates, Deduction and the Information Above these lines and this Statement refers to Federal Taxes, Rates, Deductions, Etc.

2015 California Tax Rates, Tax Tables, Personal Exemptions and Standard Deductions

The rate of inflation in California, for the period from July 1, 2014, through June 30, 2015, was 1.3%. The 2015 personal income tax brackets are indexed by this amount.

Corporate tax rates

Entity type

Tax rate

Corporations other than banks and financials

8.84%

Banks and financials

10.84%

Alternative Minimum Tax (AMT) rate

6.65%

S corporation rate

1.5%

S corporation bank and financial rate

3.5%

Individual tax rates

The maximum rate for individuals is 12.3%

The AMT rate for individuals is 7%

The Mental Health Services Tax Rate is 1% for taxable income in excess of $1,000,000.

Exemption credits

Filing Status/Qualification

Exemption amount

Married/Registered Domestic Partner (RDP) filing jointly or qualifying widow(er)

$218

Single, married/RDP filing separately, or head of household

$109

Dependent

$337

Blind

$109

Age 65 or older

$109

Phaseout of exemption credits

Higher-income taxpayers’ exemption credits are reduced as follows:

Filing status

Reduce each credit by:

For each:

Federal AGI exceeds:

Single

$6

$2,500

$178,706

Married/RDP filing separately

$6

$1,250

$178,706

Head of household

$6

$2,500

$268,063

Married/RDP filing jointly

$12

$2,500

$357,417

Qualifying widow(er)

$12

$2,500

$357,417

When applying the phaseout amount, apply the $6/$12 amount to each exemption credit, but do not reduce the credit below zero. If a personal exemption credit is less than the phaseout amount, do not apply the excess against a dependent exemption credit.

Standard deductions

The standard deduction amounts for:

Filing status

Deduction amount

Single or married/RDP filing separately

$4,044

Married/RDP filing jointly, head of household, or qualifying widow(er)

$8,088

The minimum standard deduction for dependents

$1,050

Reduction in itemized deductions

Itemized deductions must be reduced by the lesser of 6% of the excess of the taxpayer’s federal AGI over the threshold amount or 80% of the amount of itemized deductions otherwise allowed for the taxable year.

Filing status

AGI threshold

Single or married/RDP filing separately

$178,706

Head of household

$268,063

Married/RDP filing jointly or qualifying widow(er)

$357,417

Nonrefundable Renter’s credit

This nonrefundable, non-carryover credit for renters is available for:

Single or married/RDP filing separately with a California AGI of $38,259 or less.

The credit is $60.

Married/RDP filing jointly, head of household, or qualifying widow(er) with a California AGI of $76,518 or less.

The credit is $120.

Miscellaneous credits

Qualified senior head of household credit

2% of California taxable income

Maximum California AGI of $69,902

Maximum credit of $1,317

Joint custody head of household credit/dependent parent credit

30% of net tax

Maximum credit of $431

AMT exemption

Filing status

Amount

Married/RDP filing jointly or qualifying widow(er)

$87,627

Single or head of household

$65,721

Married/RDP filing separately, estates, or trusts

$43,812

AMT exemption phaseout

Filing status

Amount

Married/RDP filing jointly or qualifying widow(er)

$328,601

Single or head of household

$246,451

Married/RDP filing separately, estates, or trusts

$164,299

FTB cost recovery fees

Fee type

Fee

Bank and corporation filing enforcement fee

$92

Bank and corporation collection fee

$334

Personal income tax filing enforcement fee

$79

Personal income tax collection fee

$226

The personal income tax fees apply to individuals and partnerships, as well as limited liability companies that are classified as partnerships. The bank and corporation fees apply to banks and corporations, as well as limited liability companies that are classified as corporations. Interest does not accrue on these cost recovery fees.

2015 California Tax Rate Schedules

Schedule X — Single or married/RDP filing separately

If the taxable income is

Over

But not over

Tax is

Of amount over

$0

$7,850

$0.00

plus

1.00%

$0

$7,850

$18,610

$78.50

plus

2.00%

$7,850

$18,610

$29,372

$293.70

plus

4.00%

$18,610

$29,372

$40,773

$724.18

plus

6.00%

$29,372

$40,773

$51,530

$1,408.24

plus

8.00%

$40,773

$51,530

$263,222

$2,268.80

plus

9.30%

$51,530

$263,222

$315,866

$21,956.16

plus

10.30%

$263,222

$315,866

$526,443

$27,378.49

plus

11.30%

$315,866

$526,443

AND OVER

$51,173.69

plus

12.30%

$526,443

Schedule Y — Married/RDP filing jointly, or qualifying widow(er) with dependent child

If the taxable income is

Over

But not over

Tax is

Of amount over

$0

$15,700

$0.00

plus

1.00%

$0

$15,700

$37,220

$157.00

plus

2.00%

$15,700

$37,220

$58,744

$587.40

plus

4.00%

$37,220

$58,744

$81,546

$1,448.36

plus

6.00%

$58,744

$81,546

$103,060

$2,816.48

plus

8.00%

$81,546

$103,060

$526,444

$4,537.60

plus

9.30%

$103,060

$526,444

$631,732

$43,912.31

plus

10.30%

$526,444

$631,732

$1,052,886

$54,756.97

plus

11.30%

$631,732

$1,052,886

AND OVER

$102,347.37

plus

12.30%

$1,052,886

Schedule Z — Head of household

If the taxable income is

Over

But not over

Tax is

Of amount over

$0

$15,710

$0.00

plus

1.00%

$0

$15,710

$37,221

$157.10

plus

2.00%

$15,710

$37,221

$47,982

$587.32

plus

4.00%

$37,221

$47,982

$59,383

$1,017.76

plus

6.00%

$47,982

$59,383

$70,142

$1,701.82

plus

8.00%

$59,383

$70,142

$357,981

$2,562.54

plus

9.30%

$70,142

$357,981

$429,578

$29,331.57

plus

10.30%

$357,981

$429,578

$715,962

$36,706.06

plus

11.30%

$429,578

$715,962

AND OVER

$69,067.45

plus

12.30%

$715,962

Individual Filing Requirements

If your gross income or adjusted gross income is more than the amount shown in the chart below for your filing status, age, and number of dependents, then you have a filing requirement.

Filing Status

Age as of December 31, 2015*

California Gross Income

California Adjusted Gross Income

Dependents

Dependents

0

1

2 or more

0

1

2 or more

Single or head of household

Under 65

$16,256

$27,489

$35,914

$13,005

$24,238

$32,663

65 or older

$21,706

$30,131

$36,871

$18,455

$26,880

$33,620

Married/RDP filing jointly or separately

Under 65 (both spouses/RDPs)

$32,514

$43,747

$52,172

$26,012

$37,245

$45,670

65 or older (one spouse)

$37,964

$46,389

$53,129

$31,462

$39,887

$46,627

65 or older

(both spouses/RDPs)

$43,414

$51,839

$58,579

$36,912

$45,337

$52,077

Qualifying widow(er)

Under 65

N/A

$27,489

$35,914

N/A

$24,238

$32,663

65 or older

N/A

$30,131

$36,871

N/A

$26,880

$33,620

Dependent of another person (Any filing status)

Under 65

More than your standard deduction

65 or older

More than your standard deduction

* If you turn 65 on January 1, 2016, you are considered to be age 65 at the end of 2015.

PLEASE NOTE THAT I HAVE COMPILED THIS INFORMATION FOR AN EASY PLACE TO LOOK UP AND REFER TO THE DATA. I BELIEVE IT ALL TO BE CORRECT BUT I AM NOT RESPONSIBLE FOR ANY TYPOS. THIS PAGE IS FOR INFORMATIONAL PURPOSES, PLEASE SPEAK WITH YOUR TAX EXPERT/PREPARER WHEN MAKING TAX DECISIONS. THIS PAGE SHOULD NOT BE CONSIDERED TAX ADVICE.

The past week has been rough for the market. The below picture shows how rough a typical year is. The average peak decline in a calendar year is about 14%. So while we have hit a rough patch this week, its relatively normal for most calendar years.

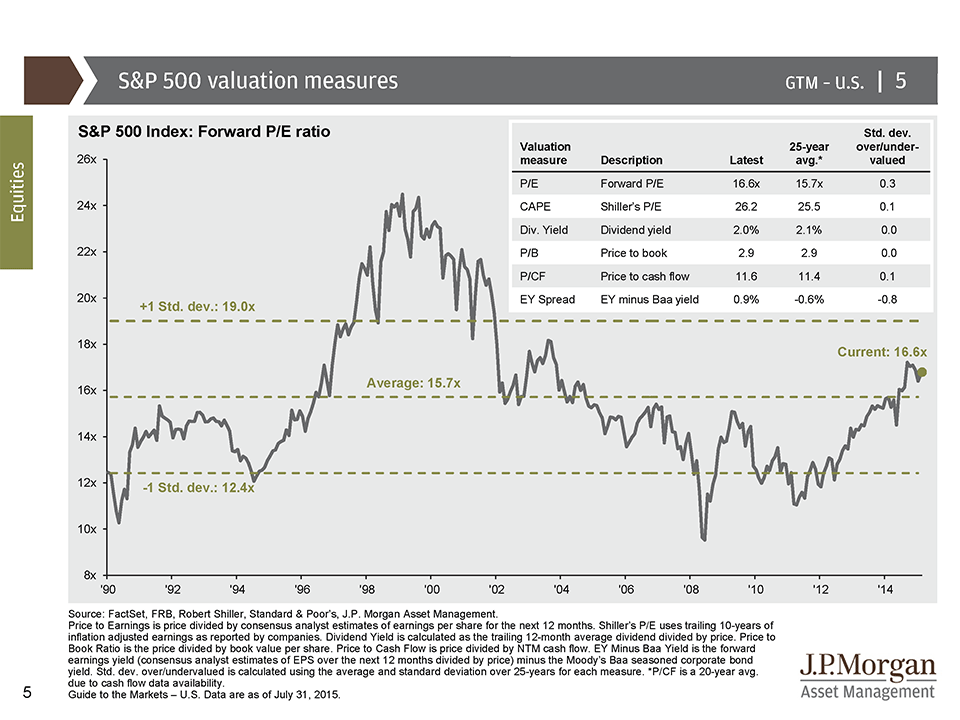

Current Market Valuation Measures – Hint – Market is Fairly Valued

The second slide attached shows the “standard deviation” of current vs historical valuation measures. While they are all slightly higher (meaning the market might be slightly overvalued), the standard deviation of almost 0 indicates that the market is fairly valued and almost completely normal relative to the historical average. The media seems to keep saying the market is over-valued lately but the statistics say otherwise.

P/E Ratio is Poor Predictor of Short Term Performance but much better at Intermediate Performance

The third slide, shows that if we look at the P/E ratio (price to earning), it is a terrible measure at predicting the next 12 months of performance for the stock market. In statistics, the R Squared measure explains how much of the next 12 months is explained by the P/E ratio. It comes in at a miserable 9% meaning that its useless for predicting short term performance. Interestingly, the P/E ratio is a better measure for longer period performance. The P/E ratio over 5 year periods helps explain 43% of performance of the subsequent years performance. Further, at the current P/E ratio, we would expect the market to be positive and not much different than historical returns for the market. (Current P/E is about 16.6).

Market Timing and Why the Average Investor Loses

These pull backs often cause fear and investor might sell after a drop. Is this a real danger?

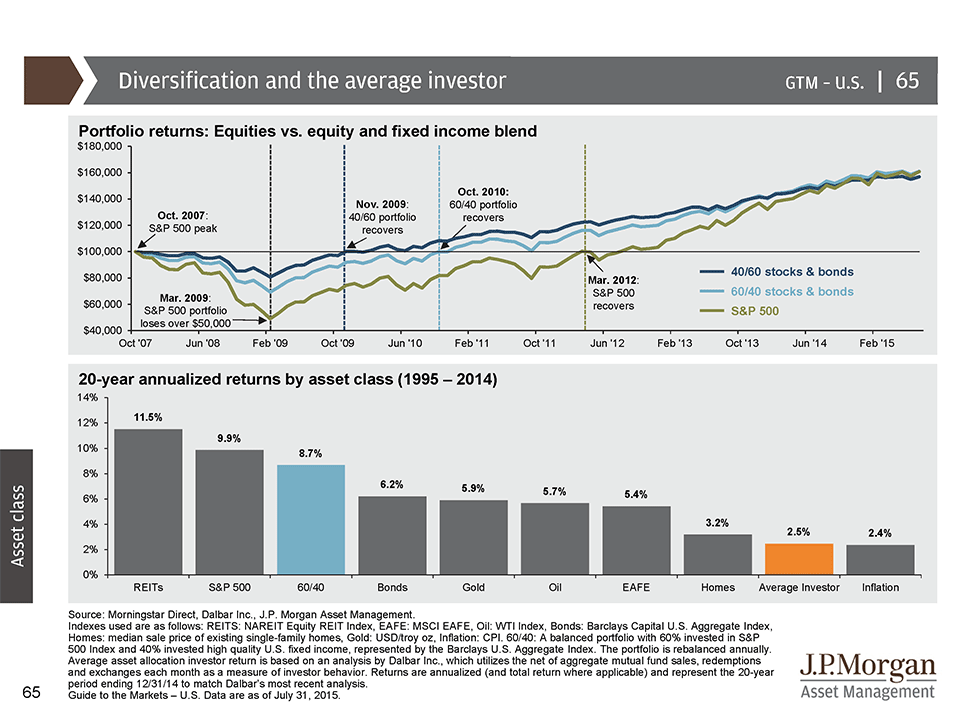

The simple answer is yes. In my opinion, the next slide shows that the average investor sells stocks when they get scared and buys stocks when they are comfortable. It helps explain how the average investor has managed to under perform nearly every asset class returning 2.5% and barely beating inflation which returned 2.4%. If there is any chart that shows the danger of market timing, its the one below.

I know your next question. You are going to ask me if investors recently have learned their lessons better? Well, on to the next chart:

Yikes! From 2009 until 2012, the retail investor has been selling their equities missing out on much of the recent run up in the market. In 2013, nearly 5 years after the financial crisis of 2008, the retail investor finally returned to the stock market. Further, the retail investor has been selling their stocks and buying bonds. Looking at institutional investors (pensions funds, endowments, etc), we see that they mostly have been adding funds to US equities as the retail investor has been selling.

So despite the relatively common knowledge that timing the stock market is difficult, retail investors continue to be late to party on bull markets, and will likely sell their stocks after the market drops, again showing that timing the market can be hazardous to your retirement goals.

Tolerating volatility is difficult and why it is critical to build a portfolio that will allow you to ride out challenging periods in the stock market.

The Take Away or Lesson from this Post?

What is our takeaway from this? Market declines in a year are very common even in years that end up with good positive performance. Market Valuation measures are not screaming that the market is over or under valued but rather that its a pretty boring fairly valued. Lastly, valuation measures are poor guides for short term performance, so we should be careful about making knee jerk reactions to numbers and stories we hear in the media.

And the Final Reminder – While we try to look at markets rationally, they simply are not rationale in the short term. If investors start to panic and start selling equities and they witness this downturn, we certainly can see a much bigger drop. However, if the fundamentals stay strong, it should prove to be another bump in the road. Pullbacks similar to this are healthy for the market to remind investors that the stock market is risky.

I would like to thank JP Morgan for their always excellent quarterly guide to the markets where the slides came from.

** The information on this website is intended only for informational purposes. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.

Investor Protection – The Department of Labor – Advisors Should Act in Your Best Interest – I Agree!

The department of Labor has an article where they are blunt about investment advice that involves a conflict of interest. As you know, I am a fee-only advisor precisely because of the Department of Labors Concerns and:

1) I am a fiduciary that will act in your best interest

2) I LOVE being able to tell people that regardless of what investment product I recommend, my compensation does not change. It is liberating to be able to choose the best product without regards to how I get paid. My compensation/fee is easy to calculate, understand, and is completely transparent. You know exactly what you are paying for.

and here is a video they embedded in the article. Please note that this video is the department of labor’s video and not mine but it demonstrate the potential conflict of interest for some advisors.

How is a fee only Advisor Different than the Video?

Simple! We get paid ONLY the fee agreed upon by the client. We then seek out the best pricing for the investment product we use. We have an incentive to locate the best product for you, without the bias of how much we will get paid.

What Should You Do? Investigate if Your Advisor is Working in Your Best Interest

1) Ask if your advisor makes a different level of compensation depending on the product they recommend

2) Ask your advisor how they are paid. If you are paying a fee, ask if that is the ONLY compensation they receive related to your accounts

3) Ask if your advisor is a fiduciary and will always act in your best interests. In my investment advisory and financial planning contracts I am a fiduciary and am contractually obligated to act in my client’s best interest and disclose any and all conflicts of interest.

** The information on this website is intended only for informational purposes. Investors should not act upon any of the information here. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.

Image by Stuart Miles at FreeDigitalPhotos.net. Video from the US Department of Labor

In this article covering investor protection we look at “titles” for advisors. One trend that investors should be cautious of is the creation of designations or titles in the finance world that imply expertise in financial planning for seniors and retirees. These “Retirement Designations” should be viewed with caution.

There Are Few Legitimate “Senior or Retirement Designations” that are meaningful

While at first it may appear that someone that is a “specialist” in the retirement planning or senior planning is exactly what you need if you are a retiree or a senior, the truth is that there are few, if any, rigorous designations or official specializations that I am aware of.

Massachusetts Has Banned Bogus Senior Designations Since 2007

LPL Financial, which is based in Boston, has been fined $250,000 after state regulator said its advisors were using titles and designations that didn’t measure up. Secretary of State William F. Galvin actually said that 10 different senior designations were used that violated the state law which has been in effect since 2007.

William F. Galvin states:

“In these days when workers are increasingly having to assume responsibility for their retirement savings, it is vital that the financial services industry not employ titles that suggest an expertise in advising senior citizens when none exists…..That is why Massachusetts has these rules in place.” – William F. Galvin Secretary of State Massachusetts.

AARP Provides Recommendations to States to Prevent the Misleading Use of Senior Designations

The AARP’s Public Policy Institute has released a 6 page recommendations to States to help curtail the misleading use of designations. You can read the recommendations here:

“The Securities and Exchange Commission and the Financial Industry Regulatory Authority (FINRA) do not endorse professional designations or titles such as “senior specialist” or “retirement advisor” that some financial professionals use to market themselves.

The requirements for being designated as a “senior specialist” vary greatly. In some cases, a financial professional may need to pass several rigorous exams and have several years of experience working in a particular field to receive a specialist designation. Other “senior specialist” designations may be relatively quick and easy to obtain, even for an individual with no relevant experience” – Securities and Exchange Commission

The Take-Away

While outside of Massachusetts, Advisors can use senior and retiree specialist titles but the investing public should take these titles with a grain of salt. The CFP designation and CFA Charter demonstrate much higher levels of experience and training than the other titles. Both programs go into great details on investing and financial planning for seniors and retirees. Further, I question the wisdom of a program offering those designations when the SEC and state regulators have specifically called out that type of designation.

** The information on this website is intended only for informational purposes. Investors should not act upon any of the information here. Reh Wealth Advisor clients should discuss with their advisor if any action is appropriate.